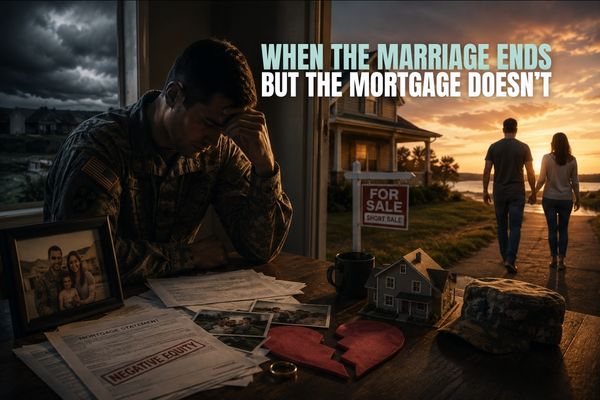

Divorce & The VA Loan: How to Untangle Your Mortgage When You Split

Divorce is emotionally draining. But when you add a home with negative equity and a VA loan into the mix, it can become financially paralyzing.

We often see military couples who are separating and stuck in a dangerous stalemate:

Neither spouse can afford the mortgage payments alone.

The house is worth less than what is owed, so they can’t just "sell it and split the profit."

They are terrified that a foreclosure will ruin both of their credit scores and the Veteran’s security clearance.

If you are navigating a divorce in Eastern NC and the house is underwater, a VA Short Sale might be your cleanest exit strategy. Here is why.

1. The "Two Households" Problem

When you were married, your dual incomes (or BAH + income) likely supported the mortgage. Now, you are trying to support two separate households (two rents, two sets of utilities) on the same income.

The math rarely works. The VA recognizes "Divorce" (and the resulting loss of household income) as a valid hardship. You do not have to wait until you have missed payments to apply for help. You can be proactive.

2. Protecting the Veteran’s Entitlement

A common mistake in military divorces is letting the ex-spouse "keep" the house without refinancing.

The Trap: If the ex-spouse keeps the house but doesn't refinance (which they often can't do if there is no equity), the Veteran’s VA Entitlement remains tied up in that property.

The Consequence: The Veteran cannot buy a new home for themselves because their entitlement is "stuck" with the ex.

The Solution: A Short Sale sells the property completely. It gets the Veteran’s name off the title and the loan, freeing them to move forward.

3. What If My Ex Won’t Sign?

This is a common hurdle. Since North Carolina is a "marital interest" state, and if both names are on the deed, both must sign to sell the home.

If your ex-spouse is refusing to cooperate, or is living in the home without paying the mortgage, you are at risk of foreclosure.

We can often work with your divorce attorney to show the other party that a Short Sale is in their best interest too (avoiding a foreclosure on their record).

4. A "Clean Break" for Everyone

A foreclosure drags on for months or years and leaves a mess of legal judgments that can tie you together financially long after the divorce papers are signed.

A VA Short Sale provides a defined end date.

The house is sold.

The debt is settled.

The tie is severed.

You can both walk away with your credit salvageable and your future unburdened.

The Bottom Line

Do not let the house become a weapon in the divorce. It is a sinking asset. The faster you liquidate it, the faster you can both heal and move on.

Discreet & Private Consultation We know this is a sensitive time. We can speak with you (and your attorney if needed) to discuss your options for exiting the home gracefully.